")

")

")

{kind=link}

Hidden Edge: India Corporate Tax Rate & 2026 FDI

Let’s be blunt. Over the last five years, each founder I have talked to has been staring at his/her product and the other one at their compliance dashboard. It is not a matter of whether we can build it or not. It is Can we develop it here and still make it work to our global investors?

The world capital market is high-stress as we head into 2026. Investors are not seeking growth only, but they are searching efficiency. And that is where that apparently terribly dull statistic, the India corporate tax rate, just gets to be the most thrilling thing on your pitch deck.

This is not the talk of policy-wonks. This is about your runway. This is about your valuation. This is regarding whether it is that Singapore or Silicon Valley VC who signs the term sheet.

Over the years founders and foreign funds have been engaged in a complicated game of cat and mouse structuring. The Singapore Flip (the establishment of a Singapore holding company) turned into a default. Why? Since India was considered a high-tax, high-friction environment.

However the basis has changed. The policy modifications introduced in the recent years are already fully cooked, and the statistics are becoming unignorable. This article is not a government press article; it is an analysts analysis of how this new Corporate tax environment is developing foreign investment in India 2026 and what you as either a founder or an analyst need to do with it.

The Welcome Mat Analogy: Why Tax is Not Only a Number.

I always inform my customers: consider the corporate tax rate of your host country as the welcome mat to the front door to your business.

When the Corporate tax rate is low and clear and stable, it conveys a message that, Welcome, we are open to business and we will not stumble you. It signals partnership.

A high, complicated, or (worse still) unanticipate rate is a mat with holes on it. Investors will be shy because they will be afraid of getting embroiled in compliance problems or losing their returns through a sudden change of policy.

The mat in the decades was a complicated thing in India. It was overloaded with surcharges, cesses as well as with the much feared Dividend Distribution Tax (DDT). Investors hated the DDT. It was as though it was taxed twice and it was a nightmare to repatriate profits.

The fact that the government acted to reduce the rate of India corporate tax rate and most importantly, to eliminate the DDT was not a simple fiscal stimulus. It was a psychological shift. It was a clear and straightforward message to world capital: We are listening. We want your business. The mat is clean.”

The Global Battlefield: vs. India. The Competition

Founders do not work under a vacuum. Neither do VCs. A global fund is running the numbers when it is deciding where to put the funds of 100 million in Asia. And the impact of corporate tax on FDI is an item of significant size on the spreadsheet.

Traditionally, capital flow going to Asia had had a small number of petting zoo Singapore (global hub), Vietnam (manufacturing gem) and Indonesia (the huge consumer market). India was considered as the high potential and high-risk cousin.

Let’s look at the raw numbers.

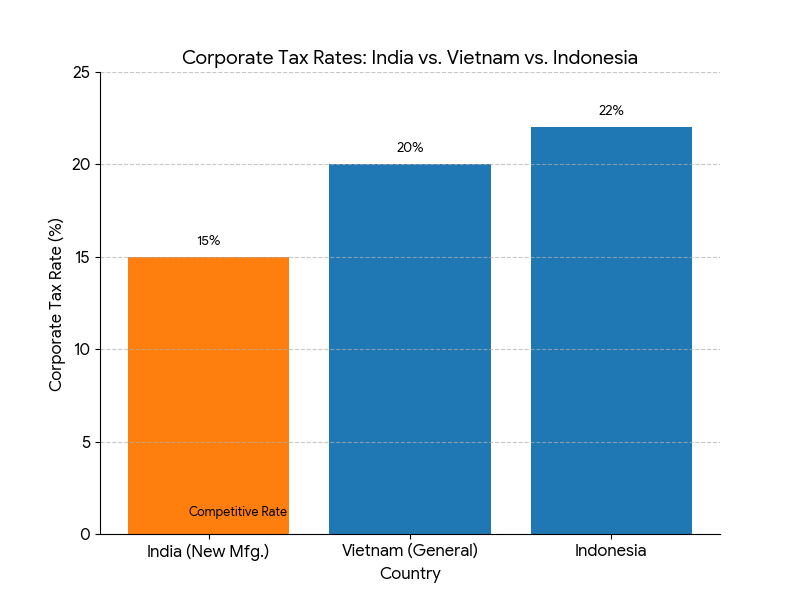

| Country | Headline Corporate Tax Rate | Key Incentives for Foreign Investors |

| India (Existing Co.) | ~22% (plus surcharge/cess) | No DDT. Stable regime. |

| India (New Mfg. Co.) | ~15% (plus surcharge/cess) | Globally one of the lowest rates. |

| Vietnam | ~20% | Multiple tax holidays and incentives, but a 20% baseline. |

| Indonesia | ~22% | Standard rate, with some incentives for specific sectors. |

| Singapore1 | ~17%2 | Low rate + extensive incentive schemes.3 |

The analysis opinion herein is as follows: It is not only about the headline rate.

- The 15% Game-Changer: When a startup has a component of Make in India, whether it is hardware, EV, deep-tech, drones, even advanced food processing, the 15 percent rate (for new manufacturing companies established after October 1, 2019) is invincible. Comparing India vs. Vietnam Corporate tax rates, now India is more aggressive as a destination to manufacture.

- The Stability Factor: It is the elimination of the DDT and the shift to a more basic regime that is making CFOs and policy analysts confident. “Are you predictable is the new gold. Capital would prefer that there be a 22% that is stable than a 17% that may vary with every turn of a political cycle.

- The “China Plus One” Tail-wind: Global supply chains. That’s a fact. Capital must have a welcome turf. The friendly part of this corporate tax structure is the competitive one. It is transforming political tail wind into financial tail wind.

This change, as recently pointed out by Economic Times has played a major role in ensuring that FDI inflows are maintained even when the world is going through a recession. It is obvious that India is not the costly outlier anymore. It is the competitive destination. The positive impact of corporate tax on FDI is clearly visible.

Tax Provisions You Can not ignore about FDI as a Startup Founder.

Alright, let’s get practical. You are a founder, you are planning your Series A, and you are negotiating with a London fund. You will have to organize your business to take advantage of the startup funding India corporate tax rate incentives.

Your CA is not just a compliance guy, he or she is your strategic partner. These are three provisions that you need in your arsenal.

1. The 80 IAC Tax Holiday: Your Three Year Profit Shield.

This is the massive one of DPIIT-recognized startups. It is a 100 percent deduction of profits on your profits over a period of three consecutive years in the first ten years of your operation.

Analyst Insight: In my experience, 9 out of ten founders at the initial stage get this wrong. They are so thrilled that they receive it in Years 2, 3, and 4, at the time of their paltry or zero profits.

Don’t do this.

This is a strategic choice. You burn your cash, construct your product, and get your market. You pull this lever when you have just reached some substantial profitability, say, Year 6, 7, and 8. You essentially enjoy three years of high profitability tax free which can be reinvested back to growth. To a VC, this enormously shortens the time to compounding returns.

2. Carry Forward of Losses: The resilience Clause.

Startups burn cash. That’s the model. We refer to the same as foreign investment in growth. The taxman calls it a “loss.”

The good news? Those losses are not an ugly figure on your P&L: Indian corporate tax law gives you an opportunity to offset future profits with these losses to business.4 With most startups (where shareholder continuity is undertaken), you can carry them forward indefinitely.

Why a US Investor Cares: When an international investor calculates their valuation model (such as a DCF), your losses as an accumulated asset turn to be a real one. They are “tax shields.”

One of my clients to whom I was dealing with SaaS had accumulated losses amounting to 2M. This was beautifully modeled when they approached their Series B raise and their new CFO did so. Their first 2M of future profits would be tax-free (on top of 80-IAC, if they did it right!). This has a direct effect of reducing the time to profitability on the model of the investor and gives you a higher present valuation.

3. SEZ / GIFT City Benefit: The Construction of a Global Hub.

Are you a global FinTech, B2B SaaS or DeepTech start-up? Do not simply establish yourself in an impersonal co-working station. You have to consider the work of Special Economic Zone (SEZ) or better yet, Gujarat International Finance Tec-City (GIFT City).

The benefits are staggering:

- Tax Holidays: The export profit holiday (excluding certain conditions) over a period of years.

- GST Exemption: GST exemption on goods/services imported to the SEZ/GIFT City unit.

- Financial Hub: There is also the development of Financial Hub Financial Hub: GIFT City, specifically, which is being made into a global financial hub, but the rules are closer to those of Singapore or Dubai than mainland India.

On one occasion, we had a FinTech customer that transferred their back-office business to GIFT City. Their effective tax rate on the export income was reduced to single digits. It is not an optimization that is a structural advantage. It informs your foreign investors that you are creating a world-first business on Day 1.

Myth vs Reality: The Busting of Mainstream FDI Tax Fears

I find the same old fears still when I speak to foreign funds. These are the sticky narratives, which are old-dated.

Myth 1: The tax system in India is still a raid Raj. It is too radical and antagonistic.

Reality: This is a 2010s problem. Look, is it perfect? No tax system is. However, the shift to faceless appraisal, the standardisation of India corporate tax rate, and the creation of the (relatively) stable GST regime has eliminated 80 per cent of the up and down. The emphasis, as may be ascertained by reading the NITI Aayog paper, has been shifted conclusively towards being action-oriented to policy-oriented incentives. [External Goal: Link to the site of NITI Aayog/applicable strategy paper].

Myth 2: “All my tax issues are resolved by my Singapore based holding company.”

Reality: Oh, the Singapore Flip. It was the default. However, in a post-BEPS (Base Erosion and Profit Shifting) world, this framework is facing a lot of scrutiny. International tax authorities such as India are operating under the tests of Substance over Form and GAAR (General Anti-Avoidance Rule).

When you have your whole company, your IP and your market in India, a shell company in Singapore is no longer the magic bullet it once was. In most instances, it is no longer less complex and risky. In many cases, it is now cheaper, cleaner and more defensible to be domiciled in India particularly with the new startup funding India tax incentives.

Myth 3: “There is something I continue to hear about, which is Angel Tax. Won’t that kill my funding?”

Reality: The reality about the angel tax (under Section 56(2)(viib)) was a true, huge headache. It was an ill-constructed regulation that penalized startups in the valuation. Nonetheless, the government has relieved big time. Startups that are recognized by DPIIT are now exempt, so long as they submit a simple declaration. The latter is a mostly resolved issue when it comes to any legitimate and well-advised startup. Fears of the past will sink your 2026 fundraising.

The 2026 Horizon: What comes next to Policy Analysts and Founders?

Where does this put us then in 2026? The direction is obvious India is leveraging its tax policy as an offensive, first-mover weapon in luring capital, and not merely a revenue collection apparatus. The comparison of India vs. Vietnam Corporate tax rates clearly illustrates this competitive shift.

For Founders: You have to quit considering tax as compliance and begin thinking about it as strategy. Your product includes your tax structure. Construct it in an efficient manner and you will have more partners. You will win foreign investment in India 2026 this way. It is not merely your MRR that you should be valued on, but your Net Profit After Tax and you control that more than you might imagine.

For Policy Analysts: It is a different game. The struggle is no longer about reducing rates. It’s “providing certainty.” The second jump will be in streamlining of the processes of administration, further streamlining GST and ensuring that the new Direct Taxes Code (when it comes) entraps this pro-growth position. The ‘Ease of Doing Business’ index is now directly linked with the ‘Ease of Paying Taxes’ as an implication of a recent RBI report on capital flows would suggest. [External Link: Citation of an RBI publication on FDI].

Conclusion: The Opportunity is Here. Are You Ready to Act?

We began with the nervousness of the founder. And finally the optimism of the analyst.

The operational modifications to the India corporate tax rate is more than just a one-time sale; it is a re-pricing of the Indian market. The risk of India that investors were taking into consideration is being systematically broken down, beginning with the P&L. Winning foreign investment in India 2026 requires a strategic understanding of these changes.

The “welcome mat” is out. It is clean, the government is keeping the door open.

To the founder who makes his homework and the investor who looks past the headlines that dates back to 1985, the opportunity is not only huge; it’s epochal. The issue is no longer whether India is a good bet, but whether your structure is good enough to go capitalize on it.

Frequently Asked Questions (FAQs)

Q1: What is the actual corporate tax rate in India for 2026?

A: It depends on your company. Most in-existent domestic companies have an effective rate of approximately 25.17% (22% base + surcharge and cess).7 New domestic manufacturing companies (established after 1st October, 2019) have a groundbreaking 17.16 (15% base + surcharge and cess). And in the case of startups recognized by DPIIT, it may be 0 on profits over 3 selected years under the 80-IAC holiday.

Q2: Does it apply to foreign companies directly to these low rates?

A: No. When a foreign company is doing business in India (e.g., in the form of a branch office), the rate is increased (around 40 percent). This is exactly the reason behind the fact that foreign investment in India 2026 nearly always enters an Indian subsidiary (a private limited company), which in turn can enjoy the advantage of the reduced domestic rates.

Q3: What is the current correlation of the India corporate tax rate with Singapore?

A: Singapore is 17% on the headline but can be significantly reduced by incentives.9 but India has 15% (effective 17.16) rate on new manufacturing and the 80-IAC holiday, which is more aggressive to new ventures eligible. The best place to be is no more a mere answer but it must be analysed.

Q4: Is the elimination of Dividend Distribution Tax (DDT) a long lasting positive one?

A: Yes. Rather than the company paying DDT, the dividend has been taxable in the hands of the shareholder.10 To foreign investors this is far better. This move alone greatly increased the appeal of startup funding India corporate tax rate incentives under the Double Taxation Avoidance Agreement (DTAA) of which they could not do with DDT.

Follow us On Linkedin, Instagram and Facebook for more content like this